“Bitcoin will be the heart of stablecoins”

By 2025, 95% of the world’s GDP will be represented by central banks exploring bitcoin, while stablecoins already move trillions. The next step in the evolution of the global financial system is for the network created by Satoshi Nakamoto to be the core of it all.

The above statement follows from a recent report, produced by industry analysts, including Eric Yakes and co-authors, who suggest that integrating the Bitcoin network into commercial and retail banking is not a futuristic dream, but a practical reality that is already taking shape.

The report’s authors highlight that banks can implement strategic upgrades to key components of their infrastructure, such as payment orchestration, digital asset custody, regulatory compliance systems, and partnerships with banking correspondents. This modularity would allow financial institutions to offer bitcoin-related services, from basic brokerage to digital asset-backed loans, payments via the Lightning Network, and private treasury solutions, without the need to rebuild their core systems.

At the core of this transformation is the modern payments hub, a technological layer that acts as a bridge between traditional financial rails and emerging networks like Bitcoin, as noted in the report.

Analysts add that this system would allow for the dynamic routing of instant transactions through Bitcoin and its 24/7 availability, advantages that traditional systems cannot match. For users, this means that banks could offer faster and more flexible services, such as international transfers or instant payments, using the pioneering digital currency as an underlying asset, which could reduce costs and improve accessibility.

Bitcoin Provides Banks with Out-of-the-Box Infrastructure

Not all banks will need to develop their infrastructure from scratch. The report underscores that the correspondent banking model, widely used in global payments, is already adapted for bitcoin. Therefore, smaller banks could partner with regulated providers, such as Coinbase, Anchorage, or even traditional institutions such as BNY Mellon, which offer custody, execution, and liquidity services.

That way, banks would focus on maintaining control over customer relationships and regulatory compliance, while delegating technical complexities to specialized partners.

In addition, the authors highlight the maturity of tools such as multisig wallets, Lightning-as-a-Service (Lightning as a Service) platforms, and MPC (multi-party computing) security facilitates this integration.

All of this allows banks to manage cross-chain assets, such as bitcoin and Ethereum-based stablecoins, with a lower technical burden. They also applaud that for users, these solutions mean greater security in the custody of their digital assets and the ability to access innovative banking services, such as bitcoin-backed loans, without compromising decentralization.

Bitcoin will be a store of value for stablecoins.

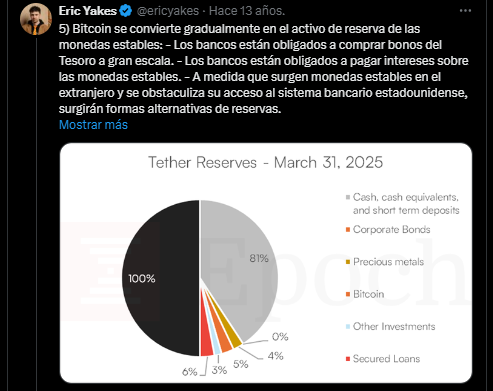

One of the key predictions in the report, backed up by Eric Yakes’ comments on social media, is that bitcoin could become the preferred reserve asset for stablecoins.

It notes that as stablecoins gain traction as a digital medium of exchange, banks are facing pressure to offer interest on these assets, similar to what happens with traditional deposits. However, stablecoins issued outside the U.S. banking system, such as offshore stablecoins, could face restrictions on access to traditional reserves, such as Treasuries.

And this is where Bitcoin comes into play, according to analysts. Yakes argues that bitcoin, as a neutral asset for currency exchange and with the ultimate settlement advantage, has the potential to replace fiat assets as a backstop for stablecoins. This change would not only diversify stablecoin reserves but could also position bitcoin as a global unit of account, especially in a context where the dollar’s dominance generates geopolitical tensions.

Although the authors do not point it out in the report, for stablecoin users, this could translate into greater stability and confidence in the use of cryptoassets, as they would be backed by a decentralized and censorship-resistant asset such as Bitcoin.

Bitcoin is at the center of the global financial system

The report and Yakes’ predictions go further by noting that in the long term, bitcoin could move from being a reserve asset to becoming the medium of exchange itself, gradually replacing stablecoins in certain transactions.

They believe that the current stablecoin proliferation is paving the way for digital signature-based payments, but that bitcoin, with its security, decentralization, and growing global adoption, will end up capturing a significant portion of this market.

Putting it into practice, directly switching to Bitcoin as a medium of exchange would offer users greater control over their funds, lower intermediation costs, and an alternative to traditional financial systems. Therefore, everyday users, this means a future in which paying with bitcoin through the Lightning network is as common as using a debit card.

However, for this whole scenario to become a reality, banks are required to balance innovation, security, and regulatory compliance, and users to adapt to a more digitized financial ecosystem. Greater financial education is also necessary for users to adopt these technologies without friction.

For analysts, bitcoin is not here to replace the financial system, but to improve it, and those who embrace this evolution will be better positioned to thrive in tomorrow’s financial world.